UAE E-Invoicing 2026–2027: Peppol Mandate, Timeline & SME Compliance Guide

MD 243 and 244 of 2025 set the UAE's e-invoicing rules: Peppol 5-corner DCTCE model, ASP-only transmission, pilot July 2026, mandatory from January 2027. Everything SMEs need to prepare.

The wait is over. On 29 September 2025 the UAE Ministry of Finance issued Ministerial Decisions No. 243 and 244 of 2025, locking in the scope, obligations, and phased timeline for the UAE's national electronic invoicing system (EIS). On 23 February 2026 the MoF published the official Electronic Invoicing Guidelines v1.0, confirming the technical fields and exchange model.

If you issue B2B or B2G invoices anywhere in the UAE — VAT-registered or not — this applies to you. Here's what's now confirmed, when each deadline hits, and what SMEs should do this quarter to stay ahead of the curve.

The Confirmed Timeline

MD 244 of 2025 sets a three-stage rollout. Dates and thresholds are no longer speculative — they are in the decision text.

- 1 July 2026 — Voluntary pilot opens for businesses that meet the technical readiness criteria and have onboarded an Accredited Service Provider (ASP).

- 1 January 2027 — Mandatory compliance for large taxpayers (annual revenue ≥ AED 50 million).

- 1 July 2027 — Mandatory for all remaining Persons Conducting Business in the UAE that fall in scope, including VAT-registered SMEs.

- Government entities follow their own onboarding track announced separately by the FTA.

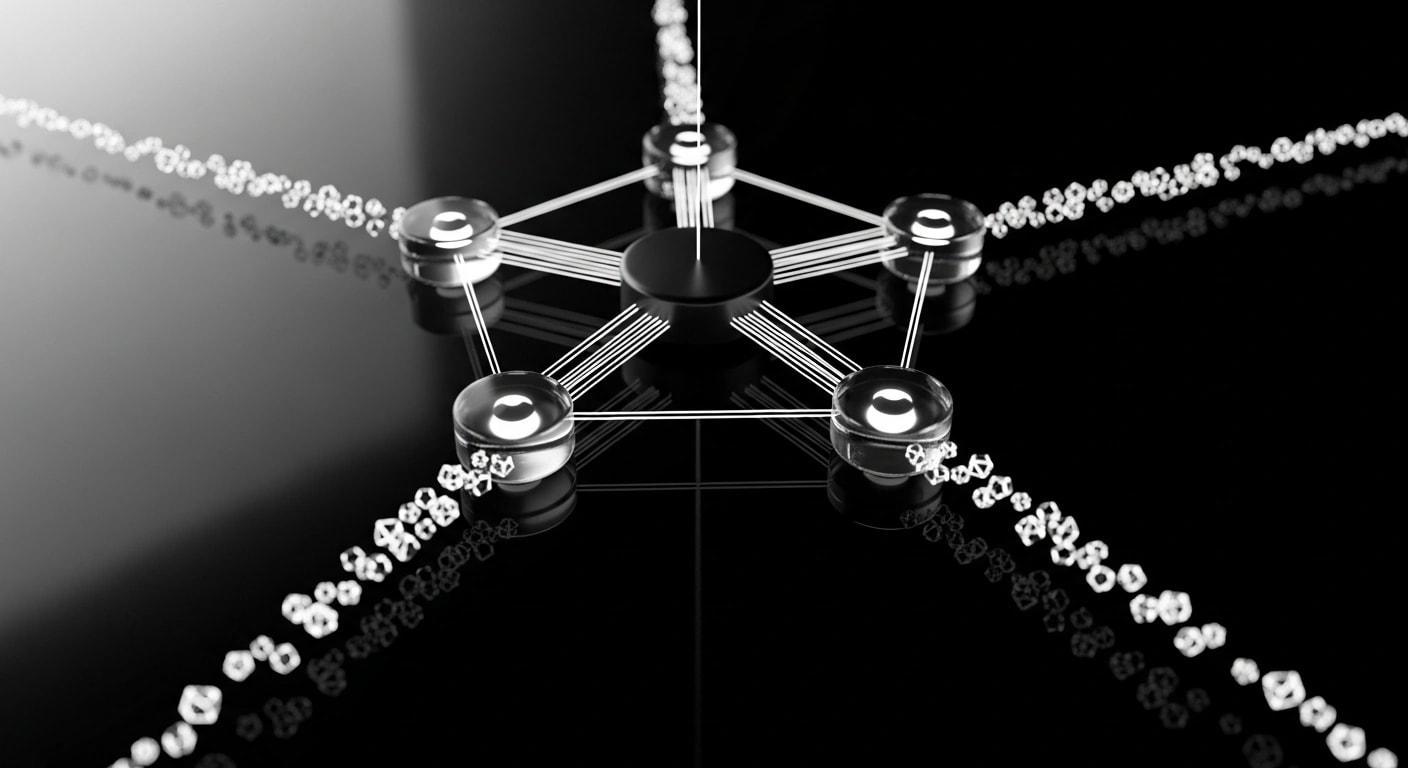

What Model the UAE Chose: Peppol 5-Corner (DCTCE)

The UAE adopted a Decentralised Continuous Transaction Control and Exchange (DCTCE) model built on Peppol — the same backbone used across the EU, Singapore, Australia, and New Zealand. In practice this is a 5-corner model:

- Corner 1 — Seller's system generates the structured invoice.

- Corner 2 — Seller's Accredited Service Provider (ASP) validates, signs, and routes it over the Peppol network.

- Corner 3 — Buyer's ASP receives and delivers it to the buyer's system.

- Corner 4 — Buyer's system ingests the invoice data directly.

- Corner 5 — The Federal Tax Authority receives a near-real-time data report from both ASPs.

Who Is In Scope, and Who Is Out

MD 243 is broad. The obligation applies to all Persons Conducting Business in the UAE — including Free Zone entities, branches of foreign companies, and non-VAT-registered businesses — whenever they engage in B2B or B2G transactions.

Explicit exclusions in the decision text:

- B2C transactions (consumer sales) — remain on current invoicing rules for now.

- International transactions where the counterparty is outside the UAE and the supply is outside the VAT net.

- Specific exempt categories the Cabinet may define (narrow and industry-specific).

What Your Invoice Must Contain

The EIS technical guidance (Feb 2026) mandates PINT AE — the UAE-localised Peppol International Invoice profile. Every issued invoice must be a structured XML document that includes, at minimum:

- Seller and buyer legal names, addresses, and Tax Registration Numbers (TRN) where applicable.

- Unique sequential invoice number and ISO 8601 issuance timestamp.

- Per-line-item description, unit, quantity, unit price, and VAT category code.

- Per-line and total VAT amounts in AED (plus invoice currency if different).

- Payment terms, due date, and — for credit notes — a reference to the original invoice number.

- The ASP's digital signature and Peppol participant identifier.

The ASP: Your Required Middleware

You cannot transmit invoices directly to the FTA. Under MD 243 and Ministerial Decision 64 of 2025 (which defined ASP accreditation criteria), every in-scope business must contract with an Accredited Service Provider. The ASP handles Peppol onboarding, schema validation, digital signing, FTA reporting, and archiving.

Practically this means your invoicing tool either is an ASP, integrates with one, or becomes irrelevant. Choose accordingly.

Penalties: The New Regime From April 2026

Cabinet Decision 129 of 2025 — effective 14 April 2026 — replaces most of the old penalty schedule. Under the new Tax Procedures Law amendments (Federal Decree-Law 17 of 2025, effective 1 January 2026), the FTA can extend audit periods up to 15 years in cases of evasion or failure to register. Non-compliance with the e-invoicing obligation will be assessed under this regime, making clean records across the 2026 transition year critical.

What SMEs Should Do Before July 2026

Even though SME compliance is technically due 1 July 2027, the right preparation window is now. Waiting for the last quarter of 2026 guarantees pain — ASPs will be booked solid and your own historical data cleanup will be rushed.

- Move off spreadsheets and Word templates. Structured data is non-negotiable.

- Audit your TRN, client master data, and sequential invoice numbering today — these fields must be clean before migration.

- Pick an invoicing platform that is already on a path to ASP integration or Peppol certification.

- Keep 100% of 2024–2026 invoice records retrievable in structured form — audit windows are expanding.

- If you carry VAT credit balances from 2021 onward, claim them now — expiry rules tighten during 2026.

How Hisabi Fits Into the Picture

Every invoice Hisabi generates is already a structured record — not a flat PDF. TRN validation, HSB-YYYY-NNNN sequential numbering, per-line VAT codes, audit trail, and bilingual EN+AR PDFs are built in. The architecture was designed with Peppol PINT AE in mind: when we complete ASP integration, your existing invoice history will map straight through, with no schema migration on your side.

Start clean now, ship-ready for 2027. Related reads: our UAE Corporate Tax SME guide and VAT Compliance for SMEs guide cover the tax side of the same compliance story.